“When a system has low complexity and we can define interactions linearly, reductionism is very useful. Many engineered systems fit this bill. A skilled artisan can take apart your wristwatch, study the components, and have a complete understanding of how the system works. Such systems also lend themselves to centralized decision making. Many companies in the industrial revolution were good examples of engineered systems-a product went down a manufacturing line, and each worker contributed to the end product. Through scientific refinement, managers could continually improve the system’s performance. On the other hand, centralized control fails for systems with sufficient complexity. Scientists call these “complex adaptive systems” and refer to the components of the system as agents. … Complex adaptive systems include governments, many corporations, and capital markets. Efforts to assert top-down control of these systems generally lead to failure, as happened in the former Soviet Union. … Thinking about the market as a complex adaptive system is in stark contrast to classical economic and finance theory, which depicts the world in Newtonian terms. Economists treat agents as if they are homogenous and build linear model-supply and demand, risk and reward, price and quantity. None of this, of course, much resembles the real world.” – from Sorting Systems, Chapter 33. The Janitor’s Dream: Why Listening to Individuals Can Be Hazardous to Your Wealth (p218)

A MULTIDISCIPLINARY PERSPECTIVE IN DEALING WITH COMPLEXITY OF THE MARKET AND THE WORLD

When you have a power blackout, who would you first call to find out about the failure? What the author did in 2003 after the major East Coast power blackout was to call his friend Duncan Watts, then a Columbia University sociology professor who has a Ph.D. in theoretical and applied mechanics and who is also one of the world’s experts in network theory. What does a power failure have to do with a sociology? Also, what does a Ph.D. in theoretical and applied mechanics have to do with a social science, you might ask? In their far-reaching discussion on the phone, the author asked what might have caused the power failure, how it progressed, and by what means could they avoid future similar events and his friend drew parallels between the blackouts, Harry Potter’s success, stock market booms, and flue epidemics. . . Can you get any clue?

According to the author, a handful of scientists-like Duncan Watts-have shown the value of multidisciplinary thinking. Physicists, psychologists, and complexity theorists have all added to our understanding of financial markets. Science offers some important mechanisms that explain how markets are efficient(and inefficient), provides important empirical results that standard finance doesn’t handle well, and shows why it’s futile to make simple cause-and-effect links in markets.

More Than You Know, published in 2008, was written in this context. The author, Michael J. Mauboussin, himself an investor, introduces and adds insights from various disciplines such as natural science, physical science, social science, and mathematics to shed lights on various facets of investment and the markets, especially the stock market. Sounds extensive? Indeed. Sounds difficult? Not so. Comprised of concise individual essays, the book is surprisingly, well actually very, enjoyable.

Even if this book is aimed at investors, investment professionals as well as corporate managers, if you have basic knowledge of financial markets such as risk and reward, you can gain further knowledge and valuable insights. If you are already an investor or a finance pundit, this book will surely broaden your mental scope and give you an intellectual stimulation in an entertaining way. What does the author want us to know more than we know?

The book is comprised of four big themes: Investment Philosophy, Psychology of Investing, Innovation and Competition Strategy, and lastly Science and Complexity Theory. Thirty-eight Individual essays are categorically placed under one of four big themes, but each essay can be also independently read. Due to large numbers of individual essays with their own distinctive topics, instead of covering them, I will briefly describe four themes first and move on to four key subjects that are repeatedly elaborated throughout the book, and therefore I considered meaningful and organize related essays into the subject where necessary. The key subjects are in below order.

- Why Diversity Matters

- The Collective Over The Individual and The Efficient Market

- The Prospect Theory, Fat Tails, Outliers, and Power Laws

- The Complex Adaptive System and The Cause and Effect Pitfalls

Investment Philosophy is firstly discussed due to its importance in investing. Even if the end result-the excess returns!-ultimately matters in investing, the author strongly believes certain disciplines such as the right process versus the outcome and sound theory building have to be in place for the long-term success and discusses about some important aspects that investors have to acknowledge such as frequency versus magnitude in expected value and loss aversion tendency. Nine essays are under this theme.

Psychology of Investing covers how sentiments or emotions can play a role in investor’s decision making individually and collectively in the market and discusses related aspects such as the affect heuristic, herding and the behavioral finance. Eight essays are under this theme.

Innovation and Competition Strategy mainly aims for investors’ thorough and comprehensive understanding of the target of their investing-i.e. the business. The author introduces various corporate strategy frameworks related with innovation and competition and discusses what strategic business analysis of an investor has to address in terms of innovation, creative destruction, competitive advantage, cooperation versus competition via the Game Theory, and growth. He also addresses certain pitfalls investors and corporate managers need to be aware in using historical P/Es, non-stationary samples and having unrealistic growth expectations. Ten essays are under this theme.

Science and Complexity Theory illustrates financial wisdom that can be gained from science-natural, physical and social-discipline. To help investors better understand the markets and investing, the author introduces various theories and adds such insights as the wisdom of the collective over an individual(expert), fat tails and outliers, the pitfall of the cause and effect thinking in understanding the markets, how complex adaptive systems and power laws are manifested in the market, how human nature is driving market swings, and how self-affinity aspect is played out in the form of fractals in return on investment. Eleven essays are under this theme.

WHY DIVERSITY MATTERS

As an investor, is having an ‘exposure to non-traditional ideas’-i.e. cognitive diversity-essential to success or just nice to have? When most occupations encourage or even insist a degree of specialization let alone finance and investment, is there any actual evidence for diversity’s value in predicting the outcomes of complex problems? According to the author, the answer is a resounding yes and he is even convinced that cognitive diversity is crucial to solving complex problems.

Two sources particularly inspired the author to think on diversity. The first is the mental-models approach to investing advocated by Charlie Munger in Berkshire Hathaway. A mental model is a framework that helps understand the problem we face, where we fit a model to the problem and not the other way-i.e. “torture reality” to fit our model. In this model, a latticework of models are constructed so we can effectively solve as many problems as possible. The author says Charlie Munger’s long record of success is an extraordinary testament to the multidisciplinary approach.

The second is The Santa Fe Institute(SFI) founded by a group of like-minded scientists who decided the world needed a new kind of academic institution. They believed much of the fertile scientific ground was between disciplines and were determined to cultivate it. The unifying theme at SFI is the study of complex systems such as human consciousness, the immune system, and the economy. SFI scientists were early in identifying the salient features of these systems and in considering the similarities and differences across disciplines.

The author was deeply inspired by their perspective on the stock market as a complex adaptive system, and this mental model made him revisit everything about finance: agent rationality, bell-shaped price-change distributions, and notions of risk and reward. Hence the importance of cognitive diversity and this book!

In the book, two essays particularly discuss about the importance of diversity in investing. The first essay, chapter 6, is on experts’ predictive ability. Using psychologist Phil Tetlock’s study on the results of experts’ predictions related to political and economic outcomes over two decades, the author emphasizes the power of diversity.

The study showed that in predictive ability, what mattered was how they thought rather than who the people were or what they believed. When we segregate the experts into two categories-the foxes and hedgehogs, foxes who know a little bit about a lot of things but not wedded to a single explanation for complex problems tend to be better predictors than hedgehogs who know one big thing and extend the explanatory reach of that thing to everything they encounter.

The next essay, chapter 28, discusses on investment intelligence and how to be an expert in a complex system such as the stock market. Quoting Norman Johnson, a mathematician, the author first presents where experts are useful and not useful.

Here is where Norman Johnson’s message is so important for investors. In well-defined systems, experts are useful because they can provide rules-based solutions. But when a system becomes complex, a collection of individuals often solves a problem better than an individual-even an expert. This means the stock market is likely to be smarter than most people most of the time, a point the empirical facts bear out. – Getting a Diversity Degree, Chapter 28. Diversify Your Mind: Thoughts on Organizing for Investing Success (p190)

In the previous essay on diversity, the fox was a better predictor than the hedgehog. But in fact these experts overall didn’t do better than the collective market in prediction. Then how to be an expert in a complex system like the stock market? Johnson suggests we need two essential features: a ‘simulation’ in the head and ‘the ability to populate our mental system with information from diverse sources.’ For the mental simulation, the author mentions George Soros’s example.

To be an expert in a complex system like the stock market, Johnson continues, you need two essential features. First, you must be able to create a “simulation” in your head, allowing you to conceive and select strategies. A description of the legendary hedge fund manager George Soros illustrates the point:

‘Gary Gladstein, who has worked closely with Soros for fifteen years, describes his boss as operating in almost mystical terms, tying Soros’s expertise to his ability to visualize the entire world’s money and credit flows. “He has the macro vision of the entire world. He consumes all this information, digests it all, and from there he can come out with his opinion as to how this is going to be sorted out. He’ll look at charts, but most of the information he’s processing is verbal, not statistical.”‘ – Getting a Diversity Degree, Chapter 28. Diversify Your Mind: Thoughts on Organizing for Investing Success (p191)

Lastly, the author quotes an article by Arthur Zeikel, former Merrill Lynch Investment Managers president on the creative personnel within the investment firm required for superior investment performance. Key traits are as below.

- Intellectually curious

- Flexible and open to new information

- Able to recognize problems and define them clearly and accurately

- Able to put information together in many different ways to reach a solution

- Antiauthoritarian and unorthodox

- Mentally restless, intense, and highly motivated

- Highly intelligent

- Goal-oriented

The author also elaborates on ‘natural decision making’ in a separate essay, chapter 16, related with this aspect. The required traits for investors in today’s fast-paced, stressful, complex markets are well described, and personally I appreciated the essay very much. Mental imagery and simulation is again highlighted and the empirical study results on experienced CFAs who are relying on this suggest the importance of this subject.

THE COLLECTIVE OVER THE INDIVIDUAL AND THE EFFICIENT MARKET

What can we learn from the behavior of social insects like bees and ants? Insights as below enable us to ponder on the power of the collective via distributed intelligence in decentralized systems.

What makes the behavior of social insects like bees and ants so amazing is that there is no central authority, no one directing traffic. Yet the aggregation of simple individuals generate complex, adaptive, and robust results. Colonies forage efficiently, have life cycles, and change behavior as circumstances warrant. These decentralized individuals collectively solve very hard problems, and they do it in a way that is very counterintuitive to the human predilection to command-and-control solutions. – Smart Ant, Chapter 29. Form Honey to Money: The Wisdom and Whims of the Collective (p194)

In two essays from chapter 29 to 30, the author elaborates on the wisdom of the collective using such examples as the decision market and the vox populi-the median estimate. And he evaluates the significance and their implications to investors.

Firstly, let’s look at the decision market. In recent years, we have seen the rise of the decision markets such as the Iowa Electronic Markets, the Hollywood Stock Exchange and BetFair, where individuals bet on outcomes of questions of interest and make or lose money based on whether or not they’re right. The author says these decision markets have proven to be uncannily accurate and, like the social insect colonies, their success relies on distributed intelligence. One significant aspect to note is that decision markets aggregate information across traders, allowing them to solve hard problems more effectively than any individual can and this is the reason why they work so well.

What do the stories about the social insects and the decision markets imply to investors? A few aspects to note according to the author.

Investors can draw a few messages from this discussion. First, decentralized systems, even with parts of limited intelligence, are often very effective at solving complex problems. The significance of distributed smarts will continue to rise as we create cheaper ways to harness the wisdom of the collective. Next, while we may be tempted to lump together all decentralized problem-solving systems, important distinctions exist-and those distinctions shape system performance. For example, stock prices tend to be efficient when investors are heterogeneous. But when heterogeneity does not prevail and investor errors become nonindependent, markets become subject to excess. Markets are more prone to excesses than colonies and decision markets. Finally, decentralized systems tend to be robust. Despite episodic excesses, markets adapt well to change. This perspective shifts the onus of rationality away from individual investors and suggests that allocative efficiency arises from the structure of local information. That’s why it is so hard to beat well-functioning markets. – Swarm Smarts, Chapter 29. From Honey to Money: The Wisdom and Whims of the Collective (p197)

As another example that proves the accuracy of the crowd, the author introduces a study done by Victorial polymath Francis Galton. In a Nature article “Vox Populi” in 1907, Galton describes a contest to guess the weight of an ox where he calculated the median estimate-the vox populi-as well as the mean. He found that the median guess was within 0.8 percent of the correct weight, and that the mean of the guesses was within 0.01 percent. The author states we have seen the vox populi results replicated over and over in such examples as solving a complicated maze, guessing the number of jellybeans in a jar, and finding missing bombs.

Companies such as Hewlett-Packard and Eli Lily tried experimentations by setting up the internal market to predict the future business and proved the vox populi was pretty good at anticipating the future.

The author emphasizes the importance of the accuracy of crowds for two reasons. First, information aggregation lies at the core of market efficiency. He defines efficiency as the inability of an individual to systematically exploit the market for superior returns. Second, companies that take advantage of the information embedded in collectives might be able to gain a competitive edge.

What does this imply to the stock market? Can we simply assume that the same rules will apply without any adjustment? How is it related with the market efficiency?

So collectives have proven adept at matching seekers and solvers and determining current or future states. How does all of this apply to the stock market? The stock market is different than the markets I’ve described because there is no answer-stocks have no specified time horizon or value. (The exception is when a company has agreed to be acquired, in which case the stock price tends to very accurately represent the ultimate value.) As a result, stock investors are susceptible to imitation because they can earn excess profits by selling to someone else willing to pay a higher price. … However, I would argue that extraordinary popular delusions and the madness of crowds are exceptions, not the rule. Investors who appreciate how and why markets are efficient will have better insight into how and why markets are inefficient. Further, investors who identify companies intelligently using collectives-the vox populi-may gain an investment edge. – And Now, For the Real World, Chapter 30. Vox Populi: Using the Collective to Find, Solve, and Predict (p202)

THE PROSPECT THEORY, FAT TAILS, OUTLIERS, AND POWER LAWS

The Prospect Theory: Frequency versus Magnitude in Expected Value

In one essay, chapter 3, under Investment Philosophy, the author emphasizes that investors have to discern the importance of frequency versus magnitude in expected value in portfolio construction. The author quotes the famous prospect theory in explaining this, but I see this principle also has to do with Fat Tails and Outliers.

Nassim Nicholas Taleb’s book, The Black Swan, well describes the peril of the magnitude(i.e. the dollar value) of the outlier(the rare black swan). Taleb is a contrarian in that he short sells when market is seemingly good. The logic of calling him a contrarian is that people don’t feel good with frequent losses from short selling when the market is good, even if one infrequent success(the black swan) can bring huge dollar gain, when the market reverses suddenly. People tend to miss that what matters is the magnitude(the dollar value) not the frequency.

This is actually what the prospect theory is about: the seemingly irrational human nature hardwired toward loss aversion. So the investors have to bear in mind this human nature but should not forget what’s more important: the magnitude.

In 1979, Daniel Khaneman and Amos Tversky outlined prospect theory, which identifies economic behaviors that are inconsistent with rational decision making. One of the most significant insights from the theory is that people exhibit significant aversion to losses when making choices between risky outcomes, no matter how small the stakes. In fact, Kahneman and Tversky found that a loss has about two and a half times the impact of a gain of the same size. In other words, people feel a lot worse about losses of a given size than they feel good about a gain of a similar magnitude. This behavioral fact means that people are a lot happier when they are right frequently. What’s interesting is that being right frequently is not necessarily consistent with an investment portfolio that outperforms its benchmark. The percentage of stocks that go up in a portfolio does not determine its performance; it is the dollar change in the portfolio. A few stocks going up or down dramatically will often have a much greater impact on portfolio performance than the batting average. – The Downside of Hardwiring, Chapter 3. The Babe Ruth Effect Frequency Versus Magnitude in Expected Value (p25)

Investors must constantly look past frequencies and consider expected value. As it turns out, this is how the best performers think in all probabilistic fields. Yet in many ways it is unnatural: investors want their stocks to go up, not down. Indeed, the main practical result of prospect theory is that investors tend to sell their winners too early(satisfying the desire to be right) and hold their losers too long(in the hope that they don’t have to take a loss). – Bulls, Bears, and Odds, Chapter 3. The Babe Ruth Effect Frequency Versus Magnitude in Expected Value (p26)

Fat Tails of the Stock Price Change Distribution

Let’s get back to the Black Swan once again. The book was published before the Financial Market Meltdown prompted by Lehman Brothers’ fall out in 2008 and people, surprised by the realization of the black swan in reality and the impact it has brought about, were talking about the black swan for quite a while. Can we say that fat tails can rule the world? Or can we say daringly fat tails change the direction of human history? Do we have any terminology explaining this-a small infrequent case with big magnitude dominates the majority of frequent cases with small magnitude? Yes, we do. It’s called the Power Law.

In chapter 31, an essay about fat tails, the author starts with Philip Anderson’s remark as below.

Much of the real world is controlled as much by the “tails” of distributions as by means or averages: by the exceptional, not the mean; by the catastrophe, not the steady drip; by the very rich, not the “middle class.” We need to free ourselves from “average” thinking. – Philip Anderson, Nobel Prize recipient in physics, “Some Thoughts About Distribution in Economics,” Chapter 31. A Tail of Two Worlds: Fat Tails and Investing (p204)

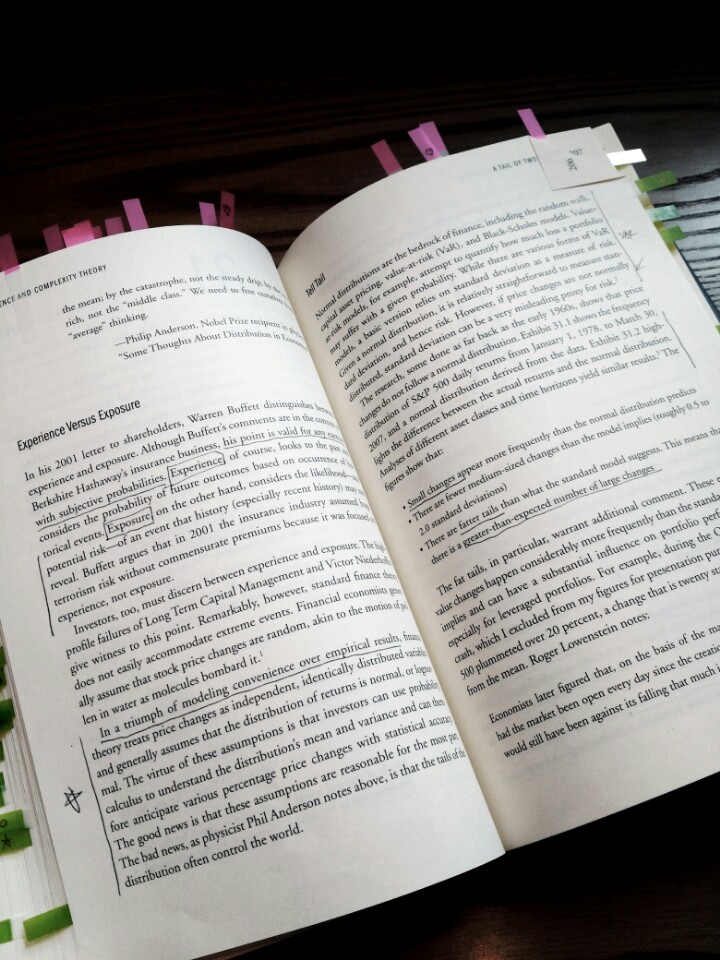

The author elaborates on standard finance theory’s limitation stemming from its convenient assumption that the stock price change is normally distributed when in reality it is more fat tailed. He argues there is a greater-than-expected number of large changes. The fat tails, these extreme value changes, happen considerably more frequently than the standard model implies and can have a substantial influence on portfolio performance-especially for leveraged portfolios.

He therefore points out what it implies to such bedrock financial theories as the random walk, capital asset pricing(CAPM), value-at-risk(VaR), and Black-Scholes models that assume the normal distribution. He claims that while it is relatively straightforward to measure standard deviation and risk given a normal distribution, if price changes are not normally distributed, standard deviation can be a very misleading proxy for risk.

Investors, too, must discern between experience and exposure. The high-profile failures of Long Term Capital Management and Victor Niederhoffer give witness to this point. Remarkably, however, standard finance theory does not easily accommodate extreme events. Financial economists generally assume that stock price changes are random, akin to the motion of pollen in water as molecules bombard it. In a triumph of modeling convenience over empirical results, finance theory treats price changes are independent, identically distributed variables and generally assumes that the distribution of returns is normal, or lognormal. The virtue of these assumptions is that investors can use probability calculus to understand the distribution’s mean and variance and can therefore anticipate various percentage price changes with statistical accuracy. The good news is that these assumptions are reasonable for the most part. The bad news, as physicist Phil Anderson notes above, is that the tails of the distribution often control the world. – Experience Versus Exposure, Chapter 31. A Tail of Two Worlds: Fat Tails and Investing (p204)

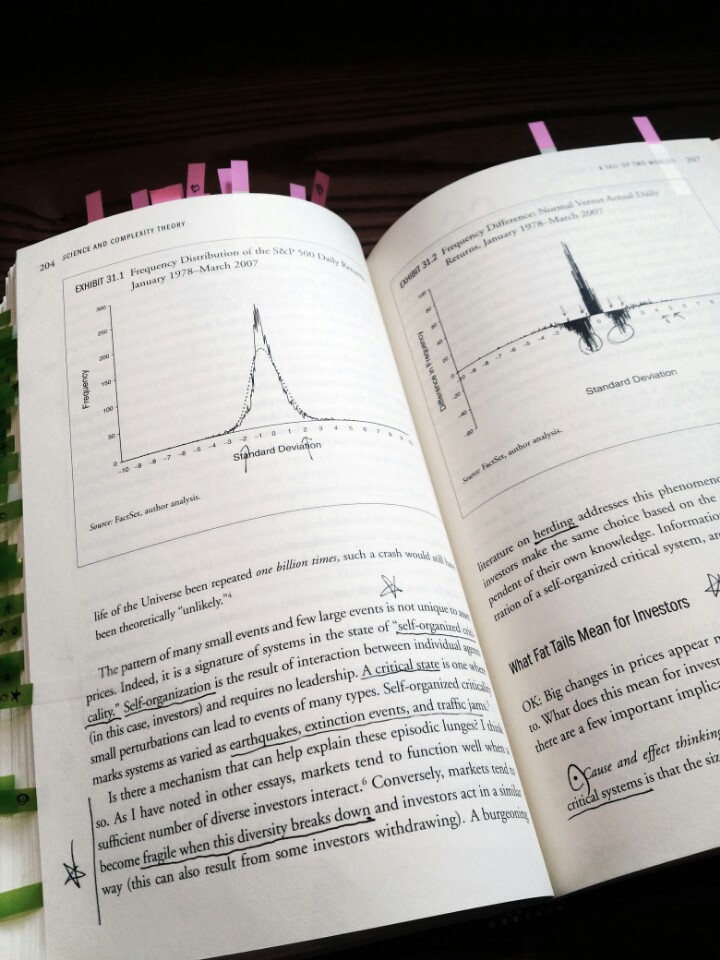

So what does this ‘fat tails’ imply for investors? The author argues the fact that big changes in prices appear more frequently than they are supposed to reflects the ‘Self-Organized Critical System’ that can also be found elsewhere. He introduces the characteristics of this system and makes a few important implications for investors and I believe they are very valuable to investors.

The pattern of many small events and few large events is not unique to asset prices. Indeed, it is a signature of systems in the state of “self-organized criticality.” Self-organization is the result of interaction between individual agents(in this case, investors) and requires no leadership. A critical state is one where small perturbations can lead to events of many types. Self-organized criticality marks systems as varied as earthquakes, extinction events, and traffic jams. … As I have noted in other essays, markets tend to function well when a sufficient number of diverse investors interact. Conversely, markets tend to become fragile when this diversity breaks down and investors act in a similar way(this can also result from some investors withdrawing). A burgeoning literature on herding addresses this phenomenon. … Information cascades, another good illustration of a self-organized critical system, are closely linked to herding. – Tell Tale, Chapter 31. A Tail of Two Worlds: Fat Tails and Investing (p206)

Big changes in prices appear more frequently than they are supposed to. What does this mean for investors from a practical standpoint? I believe there are a few important implications:

- Cause and effect thinking. One of the essential features of self-organized critical systems is that the size of the perturbation and that of the resulting event may not be linearly linked. Sometimes small-scale inputs can lead to large-scale events. This dashes the hope of finding causes and effects.

- Risk and reward. The standard model for assessing risk, the capital-asset-pricing model, assumes a linear relationship between risk and reward. In contrast, nonlinearity is endogenous to self-organized critical system like the stock market. Investors must bear in mind that finance theory stylizes real world data. That the academic and investment communities so frequently talk about events five or more standard deviations from the mean should be a sufficient indication that the widely used statistical measures are inappropriate for the markets.

- Portfolio construction. Investors that design portfolios using standard statistical measures may understate risk(experience versus exposure). This concern is especially pronounced for portfolios that use leverage to enhance returns. Many of the most spectacular failures in the hedge fund would have been the direct result of fat-tail events. Investors need to take these events into considerations when constructing portfolios. – What Fat Tails Mean for Investors, Chapter 31. A Tail of Two Worlds: Fat Tails and Investing (p207-8)

Outliers and Power Laws

There are two cases illustrated in chapter 32 that defy the normal distribution. The first is the St. Petersburg Paradox(the Bernoulli’s Game), an unsolved problem due to its infinity of expected value, presented by a mathematician Daniel Bernoulli in 1738. The next is the Fractal System elaborated by Benoit Mandelbrot, also a mathematician. These two systems don’t follow the normal distribution but rather follow the Power Law. What are the implications for investors?

According to the author, two ideas are very clear from the Bernoulli’s Game. The first is that the distributions of stock market returns does not follow the pattern that standard finance theory assumes. This deviation from theory is important for risk management, market efficiency, and individual stock selection. The second idea relates to valuing growth stocks. What are you willing to pay today for a business with a low probability of an extraordinary high payoff? The authors says this question is more pressing than ever in a world with violent value migrations and increasing returns.

Also, the implication to growth stock investing is quite important if we consider the technology industry’s winner-takes-the-most dynamics in our time. And I think this is what Peter Thiel surely meant when he said we are not living in a normal world in his book Zero to One.

Consider, for example, that of the nearly 2,000 technology-stock initial public offerings from 1980 through 2006, less than 5 percent account for over 100 percent of the $2-trillion-plus in wealth creation. And even within this small wealth-generation group, only a handful delivered the bulk of the huge payoffs. Given the winner-takes-most characteristics of many growth markets, there’s little reason to anticipate a more normal wealth-creation distribution in the future. In addition, the data show that the distribution of economic return on investment is wider in corporate America today than it was in the past. So the spoils awaiting the wealth creators, given their outsized returns, are greater than ever before. As in the St. Petersburg game, the majority of the payoffs from future deals are likely to be modest, but some will be huge. What’s the expected value? What should you be willing to pay to play? – St. Petersburg and Growth Stock Investing, Chapter 32. Integrating the Outliers: Two Lessons from the St. Petersburg Paradox (p214)

What about the Fractal System? According to the author, unlike a normal distribution, no average value adequately characterizes a fractal system because it follows a Power Law. He warns of applying traditional finance theory for this system.

Much of nature-including the manmade stock market-is not normal. Many natural systems have two defining characteristics: an ever-larger number of smaller pieces and similar-looking pieces across the different size scales. For example, a tree has a large trunk and a number of ever-smaller branches, and the small branches resemble the big branches. These systems are fractal. Unlike a normal distribution, no average value adequately characterizes a fractal system. … Fractal systems follow a power law. Using the statistics of normal distributions to characterize a fractal system like financial markets is potentially very hazardous. Yet theoreticians and practitioners do it daily. The distinction between the two systems boils down to probabilities and payoffs. Fractal systems have few, very large observations that fall outside the normal distribution. The classic example is the crash of 1987. The probability(assuming a normal distribution) of the market’s 20-plus percentage plunge in one day so infinitesimally low it was practically zero. And still the losses were a staggering $2 trillion-plus. – What’s Normal?, Chapter 32. Integrating the Outliers: Two Lessons from the St. Petersburg Paradox (p211-212)

How Power Laws Are Played Out and Its Implications to Investors

The author introduces the Zipf’s Law as a typical example of a power law and states that many scientist have discovered of this power law relationship in many other areas, since Zipf’s findings in 1930s.

Zipf’s Law, as scientists came to call it, is actually only one example among many of a “power law.” To take language as an example, a power law implies that you see a few words very frequently and many words relatively rarely. … Since his work, scientists have discovered power laws in many areas, including physical and biological systems. For example, scientists use power laws to explain relationships between the mass and metabolic rates of animals, frequency and magnitude of earthquakes(the Gutenberg-Richer law), and frequency and size of avalanches. Power laws are also very prominent in social systems, including income distribution(Pareto’s law), city size, Internet traffic, company size, and changes in stock price. Many people recognize power laws through the more colloquial “80/20 rule.” – Zipf It, Chapter 35. More Power to You: Power Laws and What They Mean for Investors (p230)

Why should investors care about power laws? The author provides three reasons. First, he states the existence of power law distributions can help reorient our understanding of risk. A power law distribution suggests periodic, albeit infrequent price movements that are much larger than the theory predicts. And this fat-tail phenomenon is important for portfolio construction and leverage. Second, it suggests some underlying order in self-organizing systems thus enables us to make some structural predictions about what certain systems will look like in the future. Lastly, standard economic theory does not easily explain these power laws. For example, neoclassical economics focuses on equilibrium outcomes and assumes that individuals are fully informed, rational, and that they interact with one another indirectly (through markets). In the real world, people are adaptive, are not fully informed, and deal directly with one another

Application-wise, how does power laws help investors? A few perspectives are presented as below and I consider the second one especially meaningful in our networked age. And this aspect has been elaborated also by Joshua Cooper Ramo in his book The Seventh Sense.

There are a number of ways that an understanding of power laws helps investors. The first way builds off Axtell’s work on company size. Given the evidence that power law distributions are robust over time, we have a good sense of what the distribution will look like in the future even though we have no idea where individual companies will fall within it. … We know ahead of time, for example, that a miniscule percentage of companies will be very large(e.g., >$200 billion sales). … Another way investors can use power laws is to understand the topology of the Internet. A classic example of a self-organizing network, the Internet has spawned a host of power law relationships-including the number of links per site, the number of pages per site, and the popularity of sites. These power laws suggest uneven benefits for companies that make heavy use of the Web. The development of the Web may be instructive for the organization of future networks. Power laws represent a number of social, biological, and physical systems with fascinating accuracy. Further, many of the areas where power laws exist intersect directly with the interests of investors. An appreciation of power laws may provide astute investors with a useful differential insight into the investment process. – Catch the Power, Chapter 35. More Power to You: Power Laws and What They Mean for Investors (p234)

THE COMPLEX ADAPTIVE SYSTEM AND THE CAUSE AND EFFECT PITFALLS

Many of science’s triumphs over the past few centuries are rooted in Isaac Newton’s principles that involve the reductionism reasoning. The small pieces, when assembled, would explain the whole. However, despite the science’s success in explaining most of the realms, we still do have certain areas where the reductionism fails to explain such as human consciousness.

Yet, even the best thinkers today have difficulty defining consciousness, let alone explaining it. Why have we had so much success in some scientific realms and so little in others, such as unveiling the mysteries of consciousness? Not all systems are alike, and we can’t understand the workings of all systems on the same level. … Many of science’s triumphs over the past few centuries are rooted in Isaac Newton’s principles. Newton’s world is a mechanical one, where cause and effect are clear and systems follow universal laws. With sufficient understanding of a system’s underlying components, we can predict precisely how the system will behave. Reductionism is the cornerstone of discovery in the Newtonian world. … The small pieces, when assembled, would explain the whole. In many systems, reductionism works brilliantly. – Beyond Newton, Chapter 33. The Janitor’s Dream: Why Listening to Individuals Can Be Hazardous to Your Wealth (p217)

If I borrow Joshua Ramo’s same argument concerning complex adaptive systems from his book, in a simple system, a plus b lead to the simple sum of c(=a+b). The parts-a and b-can explain the sum. This is what linear thinking is about. In a complex system, where a plus b don’t lead to the sum c but something else, this linear thinking fails to explain the system. We need a non-linear thinking in a non-linear world that this complex system represents.

Also, as Rifkin in his book The Zero Marginal Cost Society argues, the reason why traditional capitalist economic theory fails to explain the economic problems in our time is because of this non-linear feature of the problem in our intricately interconnected world compared to the eighteenth and nineteenth century. So, as physics-the law of thermodynamics-did explain in Rifkin’s case, the multidisciplinary approach can fill the gap.

The author mentions the characteristics of the complex adaptive system related with the stock market quite consistently throughout the book. It’s because this book is all about equity investing and the stock market. Then what’s the message here when the author says the stock market is a complex system? Our Newtonian approach with the cause-and-effect logic may not lead to finding the right solution and even lead to the poor judgment and value-destroying decisions. This is significant! Also, personally, I consider this is the core message of the author in the book.

But reductionism has its limits. In systems that rely on complex interactions of many components, the whole system often has properties and characteristics that are distinct from the aggregation of the underlying components. Since the whole system emerges from the interaction of the components, we cannot understand the whole simply by looking at the parts. Reductionism fails. … If the stock market is a system that emerges from the interaction of many different investors, then reductionism-understanding individuals-does not give a good picture of how the market works. Investors and corporate executives who pay too much attention to individuals are trying to understand markets at the wrong level. An inappropriate perspective of the market can lead to poor judgments and value-destroying decisions. – Beyond Newton, Chapter 33. The Janitor’s Dream: Why Listening to Individuals Can Be Hazardous to Your Wealth (p217)

Given its importance, let’s look into the characteristics-essential properties and mechanisms-of the complex adaptive systems.

- Aggregation. Aggregation is the emergence of complex, large-scale behavior from the collective interactions of many less-complex agents.

- Adaptive decision rules. Agents within a complex adaptive system take information from the environment, combine it with their own interaction with the environment, and derive decision rules. In turn, various decision rules compete with one another based on their fitness, with the most effective rules surviving.

- Nonlinearity. In a linear model, the whole equals the sum of the parts. In nonlinear systems, the aggregate behavior is more complicated than would be predicted by totaling the parts.

- Feedback loops. A feedback system is one in which the output of one iteration becomes the input of the next iteration. Feedback loops can amplify or dampen an effect. – Sorting Systems, Chapter 33. The Janitor’s Dream: Why Listening to Individuals Can Be Hazardous to Your Wealth (p218)

The benefits the investors gain from understanding the market as a complex adaptive systems are in two aspects as below.

The stock market has all of the characteristics of a complex adaptive system. Investors with different investment styles and time horizons (adaptive decision rules) trade with one another(aggregation), and we see fat-tail price distributions(non-linearity) and imitation(feedback loops). … Investors who view the stock market as a complex adaptive system avoid two cognitive traps. The first is the constant search for a cause for all effects. … The second trap is to dwell on the input of any individual at the expense of understanding the market itself. …. Further, studies of systems with sufficient complexity show that a collective of diverse individuals tends to solve problems better than individuals can-even individuals that are so-called experts. – The Stock Market as a Complex Adaptive System, Chapter 33. The Janitor’s Dream: Why Listening to Individuals Can Be Hazardous to Your Wealth (p219)

In the next essay, chapter 34, the author discusses about our hard-wired tendency to make links between cause and effect built through our evolution. In investing, this tendency plays out as making up stories to explain causes and effects. Quoting the Laplace’s Demon-the tempting notion epitomized by the French mathematician Pierre Simon Laplace that we can work out the past, present, and future through detailed calculation-as an example of the cause and effect bias, the author advises investors to be wary of explanations for market activity and to avoid two pitfalls as below.

Investors should be wary of explanations for market activity. Investors that actively seek explanations for the market’s moves risk one of two pitfalls. The first pitfall is confusing correlation with causality. Certain events may be correlated to the market’s moves but may not be at all causal. … The second pitfall is anchoring. Substantial evidence suggests that people anchor on the first number or piece of evidence they hear to explain or describe an event. … The stock market is not a good place to satiate the inborn human desire to understand cause and effect. Investors should take nonobvious explanations for market movements with a grain of salt. Read the morning paper explaining yesterday’s action for entertainment, not education. – Investor Risks, Chapter 34. Chasing Laplace’s Demon The Role of Cause and Effect in Markets (p227)

I have somehow managed to arrange some essays under four consistent subjects in my summary so far. Other subjects are also meaningful, and I would like to briefly mention for your reference.

- Emotions and Market Swings (chapter 12, 13, 14, 15 & 37)

- Leading or Misleading with Sample and Population (chapter 17 & 24)

- Innovation Acceleration and Faster Industry Change (chapter 19 & 21)

- Growth, Mean Reversion and Unrealistic Expectation (chapter 25, 27 & 36)

CONTEMPLATION: A COLLECTION OF AMAZING ESSAYS ON INVESTMENT AND THE MARKET

Readers! How do you feel after being exposed to non-traditional and multidisciplinary explanations about finance, investment, and the market? Aren’t they fascinating? The feel-good point about this book is the author never denies the fundamental aspect of the market-the efficient market. What he is doing is nudging us to expand our scopes to better understand the world and the market with additional and fresh tools. As mentioned, I was able to manage only a limited number of essays under a few titles for my summary, so I just feel very sad that I can’t introduce more titles with other fascinating and valuable essays. Since there are thirty-eight essays, I would like to suggest you to delve into the remaining ones if you so far enjoyed diverse aspect of knowledge and wisdom that I managed to introduce to you.

I have enjoyed several aspects about this book as below.

First, each essay is easy and short but surprisingly comprehensive in contexts and messages. And the extensiveness of the subject of each essay is awesome. And the author’s ability to contemplate on seemingly sophisticated science and investment subjects and transform them into financial wisdom with well thought-out guidance is marvelous.

Reading each of his essay under distinct subject made me think how attentive and what a great thinker the author is. Indeed, we have lots to learn from nature and science. However, not everyone can draw the same insights from the same experience or knowledge and even not everyone can deliver the insights through not-so-heavy concise essays and this is what makes the author great. I believe this is the very reason why everybody recommends this book as a must-read! Also, this can be a personal statement but I aspire to be an author like him for this reason!

Second, the book is not a serious investment manual, or strategy, or theory book. It’s a collection of essays by an erudite author and it can be enjoyed with little efforts. The author’s clear and easy narrations, enriched with well-selected quotes from famous investors, mathematicians, scientists make reading this book a pleasant journey.

Third, broad coverage of corporate strategies in the Innovation and Competitive Strategy makes reading the book absolutely rewarding. Following the book’s fourth theme-Science and Complexity Theory-which I mainly focused in my summary, this third theme-Innovation and Competitive Strategy-is the next most valuable part of the book. Why is it so? The success of your investment portfolio comes from knowing how successfully your selected stocks will perform in the future. If you don’t have a thorough picture of what’s going on in the business internally and externally, how would you know the business will create future economic value that will directly lead to your investment’s performance?

By going through this theme, I was able to expand my scope about corporate strategies and their implications for successful strategic business analysis. After all, what the author wants is investors have a thorough understanding of their objective of their investment-i.e. the business-by looking at where they are in their dynamics with peers and environment in various strategy frameworks, so that investors can achieve meaningful valuations and successful returns.

I especially liked three essays and, since I didn’t cover any essays from this theme in my summary, I would like to briefly introduce here.

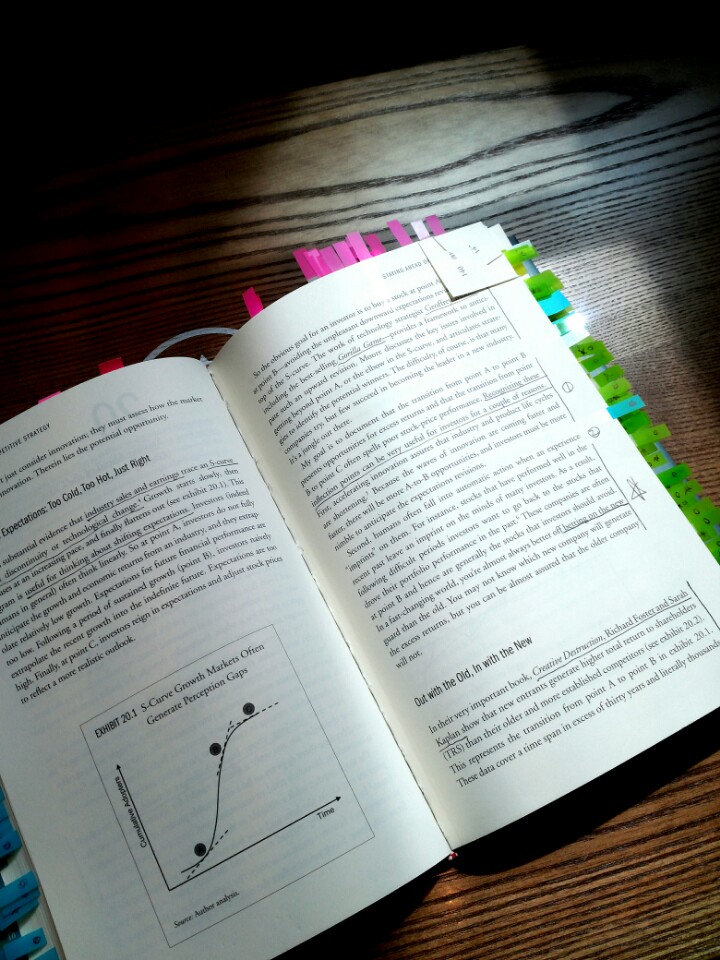

The first, chapter 20, is what creative destruction of a business can imply to investors. If an industry’s earnings and growth cycle follows an S-curve, the highest growth occurs in the inflection point and normally growth stalls at the stall point up on the S-curve. The mistakes investors make and therefore should avoid is, due to ‘imprinted’ positive experience, they tend to pick old good performers again when portfolio performance is bad, when in fact the old performer has left the inflection point and often at the stall point where growth is generally stalled.

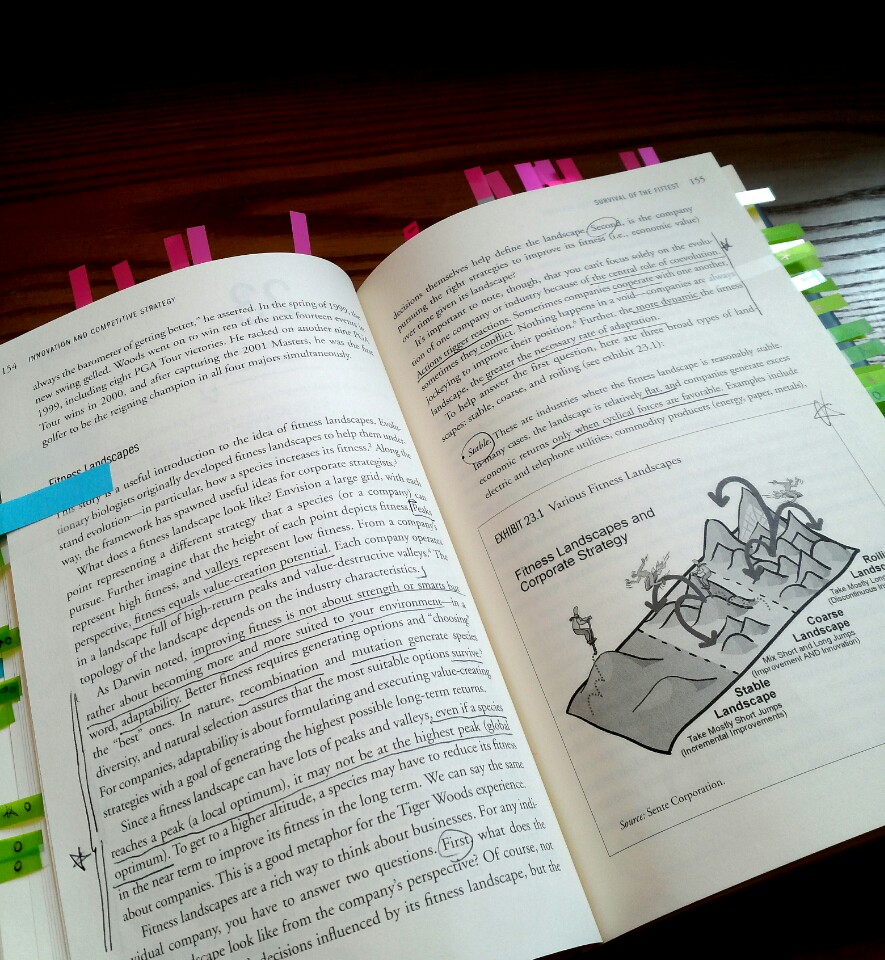

The second essay, chapter 23, compares the industry and the business’s short-term and long-term growth dynamism with a ‘fitness landscape,’ a very fresh perspective developed from evolutionary biology. From a company’s perspective, ‘fitness’ is comprised of value-creation peaks and value-destructive valleys. The topology of the landscape depends on the industry characteristics and generally we categorize the landscape into three: stable, coarse, and roiling. What it implies to the investors for strategic analysis is very insightful.

Just as different mix of short and long jumps is appropriate for different fitness landscape, so too are different financial tools and organizational structures. Traditional discounted cash flow analysis is well suited for businesses that compete in stable fitness landscape. A centralized management approach is effective, as industry activities are often clearly defined. A coarse fitness landscape requires a blend of traditional cash flow tools and strategic options. Strategic options are the right, but not the obligation, to pursue potentially value-creating business opportunities. Finally, companies that compete in roiling industries must lean more on strategic options to assess their current and potential fitness. Furthermore, these companies are well served to adopt a “strategy by simple rules” approach. This decentralized approach has agreed-upon decision rules but lets individuals make decisions at the local level as they see fit. – Tools of Trade-Off, Chapter 23. Survival of the Fittest: Fitness Landscape and Competitive Advantage (p157)

The third essay, chapter 24, discusses on the folly of using historical P/Es(Price to Earnings ratio) when the statistical properties of the population is not the same(non-stationary).

Nonstationarity is a crucial concept in any time-series analysis, and it is especially relevant for fields like climatology and finance. The basic idea is that for averages to be comparable over time, the statistical properties of the population must be the same, or stationary. If the properties of the populations change over time, the data is nonstationary. When data are nonstationary, applying past averages to today’s population can lead to misleading conclusions. … While recognition that price-earnings ratios are likely nonstationary is critical, knowing why they are nonstationary provides more practical insight. Three big drivers of price-earnings ratio nonstationary are the role of taxes and inflation; changes in the composition of the economy; and shifts in the equity-risk premium. – Nonstationarity and Historical P/Es, Chapter 24. You’ll Meet a Bad Fate If You Extrapolate: The Folly of Using Average P/Es (p161)

Fourth, I’ve very much enjoyed the complex adaptive system and power laws as explanations of the stock market. When I finished this book early this year, these concepts didn’t imprint much to my perception on the market let alone the world. Coincidently or not, however, the books I read thereafter continuously brought up this subject in explaining, for instance, the startup and technology industry(Zero to One), network power(The Seventh Sense), and economic theory(The Zero Marginal Cost Society), opening my eyes in a short time frame. I confess that now I became an advocate to these laws. I use these frames when I observe the world we are in-the complex world where everything is interconnected than any other period in human existence.

What can we learn after all? The world is changing and advancing in unprecedented pace and is getting more and more complex. The linear thinking represented by the reductionism and the cause and effect is no longer able to explain social and natural phenomena coming out of complexity due to advanced technology and ever-wider connection and we need new ways of thinking in approaching problems and solutions. As the world, including the financial market, is getting rearranged and restructured on the networked world, I believe the multidisciplinary approach will tremendously help us understand and solve many problems let alone predict for the future. And I believe this is what the author intended!

CLOSING

You’d better know more than you know in our complex world. Well thought-out and neatly presented, this investment book is a must read to investors especially for equity investors. If Jim Rogers’ Street Smarts highlighted the importance of history and philosophy to know yourself and the world better, More Than You Know highlights the importance of diverse set of knowledge and thinking process through the wisdom gained from multidisciplinary perspectives to know the market and the world better. If the former was rather about the big pictures and flows throughout time(history), the latter is rather about deepened perspective to understand the inner workings of the nature, the society and the investment universe with technicality of finance and investment.

The broad scope of covered subjects with deep insights the author brings are wonderful. I would say this book is an intellectual feast on investing. It will surely expand your mind and thought process to effectively deal with complex problems. Even better is you can read it light-heartedly.

WHO SHOULD READ THIS BOOK:

Investors. Finance and Investment Professionals. Corporate Executives. Financial Analysts. CFAs. Economists.

RATING: 5 out of 5

RECOMMENDED CATEGORIES:

Business, Investment, Finance, Economics, Natural Science, Social Science, Mathematics, Physical Science.

ABOUT THE BOOK

Author(s): Michael J. Mauboussin

Published: 2008(expanded version), USA

Publisher: Columbia Business School

Hard Cover, 257 pages