Summary ->> CONTEMPLATION ->> CLOSING

III. PROMISE VERSUS AS-IS

We are observing exponential technological progress made on top of exponential technology development today. For this reason, what the authors observed and saw as a promise may be different as of today.

Out of many revolutionary promises the authors elaborated, my key interest and enthusiasm first of all, was whether micropayments will be indeed possible. I loved the ideas of economic inclusion of those billion people who are excluded from banking let alone the Internet.

During my research, however, I have found some of the authors’ assertions hence possibilities have changed or evolved into a different direction. I am listing a few of them for future readers not to get misled by the promise that may not be valid as of today. I will discuss in the form of questions and answers.

PRIVACY

Q: Does the blockchain technology indeed protect privacy as the authors assert? Is Bitcoin indeed anonymous?

A: Not necessarily. It leaves a trail and pattern.

Some have proven over the years that Bitcoin is not anonymous. One of security researchers claims using bitcoin “leaves patterns behind that sophisticated math can follow pretty easily. But that doesn’t mean that it doesn’t have value to transaction security and user privacy, even in its pseudonymous state. 124

Many existing DLT systems use pseudonymous ledgers, where individuals are represented by addresses rather than their real-world identities. However, this is not the same as true privacy; a number of studies have demonstrated that a lot of information can be determined by analyzing such pseudonymous ledgers. 125

SECURITY

Q: Does the blockchain technology indeed guarantee security?

A: Not necessarily. It can be penetrated.

Central control, as in a single administrator, can also be a double-edged sword since a single point of control is also a single point of failure. Blockchain technology is exactly the opposite: its distributed nature also makes it a potential security threat.

In the enterprise, centralized control can translate into security. With blockchain, which is decentralized, the technology works best when information sharing is a necessity across multiple, often disparate, parties. If you want to hack, you wouldn’t just have to hack one system like in a bank… you’d have to hack every single computer on that network, which is fighting against you doing that. However, several computer scientists believe it can be penetrated. 126

When requested for an interview, one of the author, Alex Tapscott, the CEO and founder of Northwest Passage Ventures, said while no system is “unhackable,” blockchain’s simple topology is the most secure today. “So again, not unhackable, but significantly better than anything we’ve come up with today,” Tapscott said. 127

Also, like everything else of value running on computers, Bitcoin, other cryptocurrencies, and blockchains have come under frequent successful attacks. Hundreds of millions of dollars have been stolen, people have been cheated, and blockchains ripped off. 128

BANKS’ AND BUSINESSES’ INTEREST ON PERMISSIONED BLOCKCHAIN

Q: Are banks and other large enterprises as enthusiastic on the blockchain technology as the authors claimed?

A: No. Interests are waning due to limitation of private blockchains.

Many traditional businesses, including Wal-Mart, Nasdaq, and JPMorgan Chase, have been showing interest (and investing big bucks) in using blockchain technology to create private record systems. 129

But not all blockchains are created equal. Bitcoin’s built-in economic incentives ensure that hundreds of thousands of daily transactions are logged and verified on its public ledger. Private enterprises employing blockchain technology without a similar verification structure, experts say, run the risk of handicapping reliability and consumer security.130

For example, even though more than 60 banks and large enterprises announced that they would invest in R3 CEV, a consortium to build a private blockchain for the financial industry in 2016, since then several banks, including Goldman Sachs and Banco Santander, have pulled out. And five others, including JPMorgan Chase, are rumored to be backing out of participation in its current $150 million funding round as of 2017. 131

These moves could signal that private blockchains are struggling. Companies that traditionally keep their customer data under tight lock and key are understandably uneasy about adopting, let alone investing in, technology that would force them to “share a ledger of transactions. 132

Secondly, it is claimed that maintaining a blockchain is no trivial matter in terms of required cost. “All partners of a consortium blockchain are bearing the costs of all the other participants,” he says, a redundancy that makes the network even more expensive to maintain, as more data is recorded. Also, off-loadingdata to a repository that links back to the active blockchain would be just as risky as employing a traditional data warehouse. 133

Thirdly, as of 2017, more than 15 members of blockchain consortium Hyperledger also have either cut their financial support for the project or quit the group over the past few months, according to documents seen by Reuters. 134

The weakening support for Hyperledger from some large members highlights how large firms have become more selective with their blockchain efforts as the technology matures. As mentioned, JP Morgan Chase left R3, following the departure of Goldman Sachs, Banco Santander and others in early 2017. 135

Importantly, despite the excitement, blockchain is not yet used to run any large scale projects 136

INITIAL COIN OFFERINGS (ICOs)

Q: Is ICOs new alternative to traditional IPOs?

A: They are different. You don’t receive equities hence voting rights in the start-up you invest through ICOs.

ICOs are the Wild West of financing — they sit in a grey zone where the U.S. Securities and Exchange Commission (SEC) and many other regulatory bodies are still investigating them. 137

The main problem is, that most ICOs don’t actually offer equity in start-up ventures; instead, they only offer discounts on cryptocurrencies before they hit the exchanges. Therefore, they don’t fit into the current definition of a security, and are technically outside of traditional legal frameworks. 138

Secondly, they are global instruments — not national ones — and they are funded using Bitcoin, Ethereum and other cryptocurrenciesthat are not controlled by any central authority or bank. Anyone can invest, and they can even do so pseudo-anonymously (it’s not impossible to find out who people are, but it’s not easy, either). 139

Then why are Venture Capitals becoming more interested in ICOs? It’s mainly because of the liquidity. Rather than tying up vast amounts of funds in a unicorn startup and waiting for the long play — an IPO or an acquisition — investors can see gains more quickly, and can pull profits out more easily, via ICOs. They simply need to convert their cryptocurrency profits into Bitcoin or Ethereum on any of the cryptocurrency exchanges that carry it, and then it’s easily converted to fiat currency via online services such as Coinsbank or Coinbase. 140

Also, using ICO’s unregulated feature and easy possibility of quickly cashing out through exchanges, some scammers are luring investors without proper white paper or clear business plans into funding.

MICROPAYMENTS

Q: Are micropayments indeed possible?

A: No. Micropayments currently are impossible. The transaction fees are too high.

Bitcoin was once touted as a cheaper alternative to credit cards that was going to revolutionize the payments industry, but the P2P digital cash system has hit a bit of a speed bump in terms of those long-promised “free” transactions. 141

Bitcoin payments were much cheaper in the past because demand for block space was much lower. Users are now essentially “bidding” on the right to have their transactions included in the next block. Large-value transfers and payments that necessitate a certain degree of censorship resistance will tend to outbid lower-value, everyday payments such as the purchase of a cup of coffee. 142

As of 2017, it was believed that the bitcoin blockchain is basically becoming “useless” for low-value, instant purchases. If we’re ordering a beer at a bar, we’re better off using cash or a credit card at this point. 143 Solutions such as Bitcoin Lightning are in development phase, but not tested nor proven.

CLOSING

This book is full of business cases and insights about the technology. I could feel the authors’ enthusiasm about the great potentials of the new technology throughout the book.

What makes reading this book rewarding is resourcefulness. The book provides a full landscape about what’s happening in various industries, so it’s good for anyone who wants to gain further in-depth insights. Especially so, if readers already have a basic understanding about the technology and the current development.

Another good point is the authors provide a strategic perspective to future business applications. Progressive concepts of future firms in terms of decentralized organization without boundaries are difficult and mind-blowing in some sense but their strategic approach for potential opportunities and threats and for value creation is noteworthy. If any firm is considering a blockchain technology for their future business adoption, this book can provide some insight for that matter. For this reason, I have labeled this book as Business Strategy book.

However, on the flip-side, this book is not recommendable for a sheer beginner without technological knowledge. Readers need to be quite determined to fully maximize the value the authors provide. Also, certain missing perspectives such as private money issue, can mislead readers into believing Bitcoin and the bitcoin blockchain are the future. Especially so, when the authors discussed bitcoin as a potential could-have-been replacement during the latest Greek currency devaluation crisis.

Another weak point I want to mention about the book is, their in-depth coverage for almost every aspect with strategic considerations makes this book almost a plain text book that’s rather appropriate in the school. Maybe it is!

Also, this book is good to be read sooner than later. Because, as I mentioned, the technology evolves too fast these days and I found much discrepancy between the authors’ assertions and the current development in reality.

Lastly, on a separate note, due to so many variants entering into the space, I believe we need to be patient for this technology’s evolution. If this technology is to be adopted by mass as the next foundational technology, as Harvard professors claim, it will take more than a decade from now. 144

Regarding the bitcoin blockchain specifically, I believe it is surely “A Canary in the Coal Mine,” as one paper dubbed, that will surely herald lots of innovations or “Something Bigger to Come” in the coming future, and that’s good for us! 145

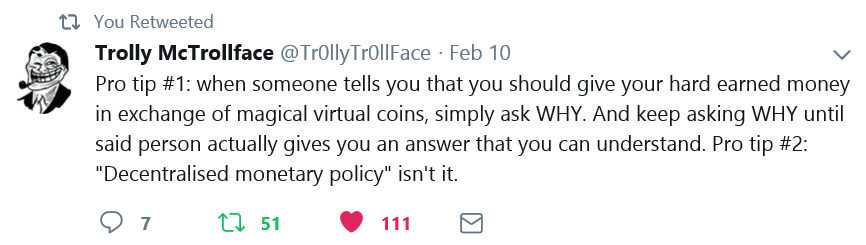

What we need to be careful is just those scammers who free ride on rising values as well as on unfamiliar novelty, promoting unrealistic dreams and magic through this new technology! Your hard-earned cash need to be spent wisely! I liked one twit message by a pseudonymous twitter user as below.

WHO SHOULD READ THIS BOOK:

Business Leaders, Entrepreneurs, Leaders in Banking and Financial Services, Anyone who wants to gain knowledge and further insights on the blockchain technology

RATING: 3 out of 5

Ideas: 3

Delivery: 3

RECOMMENDED CATEGORIES:

Business, Finance, Strategy, Technology

ABOUT THE BOOK

Author(s): Don Tapscott, Alex Tapscott

Published: 2016, USA

Publisher: Portfolio Penguin

Paperback, 311 pages