“The key point is that not all sets of institutions, when you add up the sum of the parts, are equal. There are good and bad combinations. In some sets of institutions, people can flourish freely as individuals, as families, as communities. That is because the institutions effectively incentivize us to do good things-like, for example, inventing new and more efficient ways of working, or co-operating with our neighbours rather than trying to murder them. Conversely, there are institutional frameworks that have the opposite effect: incentivizing bad behaviour … Where bad institutions pertain, people get struck in vicious circles of ignorance, ill health, poverty and, often, violence. Unfortunately, history suggests that there are more of these suboptimal frameworks than there are good frameworks. A really good set of institutions is hard to achieve. Bad institutions, by contrast, are easy to get stuck in. And this why most countries have been poor for most of history, as well as illiterate, unhealthy and bloody. … It is clearly desirable that societies with bad institutions should get better ones. … But there is a more insidious process that is going on at the same time, whereby societies with good institutions gradually get worse ones. Why is this?” – Why Institutions Fail?, Introduction, p18-19

“We humans live in a complex matrix of institutions. There is government. There is the market. There is the law. And then there is civil society. Once … this matrix worked astonishingly well, with each set of institutions complementing and reinforcing the rest. That, I believe, was the key to Western success in the eighteenth, nineteenth and twentieth centuries. But the institution in our times are out of joint. It is our challenge, in the years that lie ahead, to restore them – to reverse the Great Degeneration – and to return to those first principles of a truly free society which I have tried to affirm, with a little help from some of the great thinkers of the past.” – A Bigger Society, Chapter 4. Civil and Uncivil Societies, p134

WHY AND HOW GREAT NATIONS DEGENERATE – A Historian’s Perspective

When Adam Smith described in The Theory of Moral Sentiments about profoundly self-interested human nature by the little finger episode, in which he observed that we feel worse about the prospect of losing our little finger than we do about the death of a multitude of strangers far away, what he meant by ‘a far away place’ was China.

It appears that, in the Westerner’s eyes in the eighteenth century, the remote China was losing its growth momentum compared to the West that was growing and expanding with the Industrial Revolution.

What was happening in China?

The author, a well-known historian, often for his contrarian views, sees something is happening in the West now, things similar to what had happened in that far away empire in the eighteenth century and wants to make a case.

My book review will follow below order.

- Characteristics of a Stationary State

- The Great Degeneration: 4 Black Boxes

- Political Black Box: Debt, Democracy and the Social Contract Between Generations

- Economic Black Box: Financial Crisis, Financial Markets and Regulation

- Legal Black Box: The Rule of Law

- Social Black Box: The Civil Society

- Contemplation

- Closing

CHARACTERISTICS OF A STATIONARY STATE

In The Wealth of Nations, Adam Smith believed that a nation – in terms of its process of growth and economic development – goes through three distinctive stages: the Progressive, Stationary, and Declining State.1

In the progressive state, the process of growth is cumulative. Division of labour made possible by accumulation of capital and expansion of market, increases national income and output, which in turn, facilitates saving and further investment and in this way, economic development rises higher and higher. Smith’s progressive state is in reality the cheerful and hearty state to all the different orders to the society.

But this progressive state is not endless. It ultimately leads to the stationary state. It is the scarcity of natural resources that stops growth. An economy in a stationary state is characterized by unchanged population, constant total income, subsistence wage, elimination of profit in excess of the minimum consistent with risk and absence of net investment.

The competition for employment reduces wages to subsistence level and competition among the businessmen brings profits as low as possible. Once profit falls, it continues to fall. Investment also starts declining and in this way, the end results of capitalist is the stationary state.

When this happens, capital accumulation stops, population becomes stationary, profits are minimum, wages are at subsistence level, there is no change in per capita income and production and the economy reaches the state of stagnation. The stationary state is dull, declining, melancholy and life is hard for different sections of the society.

And ultimately life is miserable in the declining state.

The author draws attention to two significant characteristics of the stationary state and reminds the readers of their similarities in our time.

In two seldom quoted passages of The Wealth of Nations, Adam Smith described what he called ‘the stationary state’: the condition of a formerly wealthy country that had ceased to grow. What were the characteristics of this state? Significantly, Smith singled out its socially regressive character. First, wages for the majority of people were miserably low: …The second hallmark of the stationary state was the ability of a corrupt and monopolistic elite to exploit the system of law and administration to their own advantage: … I defy the Western reader not to feel an uneasy sense of recognition in contemplating those two passages. – The Stationary State, Introduction, p9-10

What did Adam Smith witness in China in the eighteenth century? It was the very characteristics of the stationary state. When countries’ ‘laws and institutions’ degenerate to the point that elite rent-seeking dominates the economic and political process, those nations arrive at the stationary state. Unfortunately, the author argues that this is the case in important parts of the Western world today. Hence the Great Degeneration.

In Smith’s day, of course, it was China that had been ‘long stationary’; a once ‘opulent’ country that had simply ceased to grow. Smith blamed China’s defective ‘laws and institutions’ – for the stasis. More free trade, more encouragement for small business, less bureaucracy and less crony capitalism: these were Smith’s prescriptions to cure Chinese stasis. He was a witness to what such reforms were doing in the late eighteenth century to galvanize the economy of the British Isles and its American colonies. Today, by contrast, if Smith could revisit those same places, he would behold an extraordinary reversal of fortunes. It is we Westerners who are in the stationary state, while China is growing faster than any other major economy in the world. The boot for economic history is on the other foot. – The Stationary State, Introduction, p10

THE GREAT DEGENERATION: FOUR BLACK BOXES

How have Western institutions indeed degenerated? The author wants to demonstrate this by opening up four long-sealed black boxes each labelled as Democracy, Capitalism, The Rule of Law and Civil Society, all four key components of our civilization. He believes these highly complex set of interlocking institutions are what makes a system work, so if it stops working, it’s because of a defect in the institutional wiring, which we need to look inside.

1. Political Black Box: Debt, Democracy and the Social Contract Between Generations

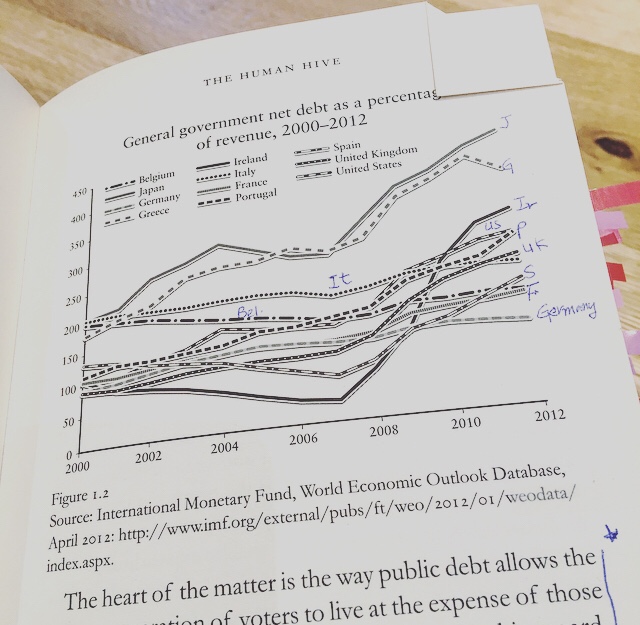

The West is slowing down. Since the outburst of the 2008 financial crisis up until 2012 as of the author’s writing, what he perceives is that the West ceased to grow. He identifies deleveraging as the explanation of the Western slowdown.

The voguish explanation for the Western slowdown is ‘deleveraging’: the painful process of debt reduction (or balance sheet repair). Certainly, there are few precedents for the scale of debt in the West today. This is only the second time in American history that combined public and private debt has exceeded 250 per cent of GDP. … In only eight was the initial debt/GDP ratio above 250 per cent, as it is today not only in the US but also in all the major English-speaking countries (including Australia and Canada), all the major continental European countries(including Germany), plus Japan and South Korea. The deleveraging argument is that households and banks are struggling to reduce their debts, having gambled foolishly on ever rising property prices. But as people have sought to spend less and save more, aggregate demand has slumped. To prevent this process from generating a lethal debt deflation, governments and central banks have stepped in with fiscal and monetary stimulus unparalleled in time of peace. Public sector deficits have helped to mitigate the contraction, but they risk transforming a crisis of excess private debt into a crisis of excess public debt. In the same way, the expansion of central bank balance sheets (the monetary base) prevented a cascaded of bank failures, but now appears to have diminishing returns in terms of reflation and growth. – Beyond Deleveraging, Introduction, p3

The West’s slowdown with deleveraging; a private debt crisis morphed into a public debt crisis; balance sheet expansion of central banks having diminishing returns in terms of growth. Out of these, the author considers the mounting public debt of our time as a degenerative feature of the political system in democracy. Why?

The author elaborates on public debts in English history as an example and compares the different nature of public debts then and now. He quotes one seminal article published in 1989 by North and Weingast, where they argue one particular institution – the Glorious Revolution – decisively altered the trajectory of English history and the real significance of it lay in the credibility it gave the English state as a sovereign borrower. From 1689, Parliament controlled and improved taxation, audited royal expenditures, protected private property rights and effectively prohibited debt default. This self-enforcing arrangement enabled the English state to borrow money on a scale that had previously been impossible because of the sovereign’s habit of defaulting or arbitrarily taxing or expropriating at the time. The late seventeenth and early eighteenth century thus inaugurated a period of rapid accumulation of public debt without any rise in borrowing costs – rather the reverse. The public debt was then used to finance wars.

What about the public debt in our time? First, according to the critics of Western democracy, the most obvious symptom of the malaise is the huge debts we have managed to accumulate in recent decades, which (unlike in the past) cannot largely be blamed on wars.

Secondly, whereas the post-crisis public discourse considers public debt issue as a problem in itself and is focused on ‘austerity’ versus ‘stimulus’ element, the author believes they are rather a consequence of a more profound institutional malfunction. He claims the heart of the matter is the way public debt allows the current generation of voters to live at the expense of those as yet too young to vote or as yet unborn.

The author identifies two distortions to note with regards to public debt of our time. First, the statistics commonly cited as government debt encompass only the sums owed by governments in the form of bonds. The rapidly rising quantity of these bonds certainly implies a growing charge on those in employment, now and in the future, since – even if the current low rates of interest enjoyed by the biggest sovereign borrowers persist – the amount of money needed to service the debt must inexorably rise. Second, the official debts in the form of bonds do not include the often far larger unfunded liabilities of welfare schemes such as Medicare, Medicaid and Social Security in the US, for example. He argues the government debt statistics are themselves deeply misleading, in this sense.

Therefore, he argues the public debt is rather a malfunction of political system of democracy in which the enormous inter-generational transfers implied by current fiscal policies are a shocking and perhaps unparalleled breach of the social contract: a partnership between generations. Edmund Burke defined: “Society is indeed a contract … the state … is … a partnership not only between those who are living, but between those who are living, those who are dead, and those who are to be born.” The author contemplates that the biggest challenge facing mature democracies is how to restore the social contract between the generations, even if the obstacles to doing so are also daunting.

Something needs to be done. How? The author suggests the way in which governments account for their finances be altered. For instance, public sector balance sheets can and should be drawn up so that the liabilities of governments can be compared with their assets. That would help clarify the difference between deficits to finance investment and deficits to finance current consumption. Governments should also follow the lead of business and adopt the Generally Accepted Accounting Principles. And, above all, generational accounts should be prepared on a regular basis to make absolutely clear the inter-generational implications of current policy.

What happens if something is not done? One potential scenario: The debt continues to mount up. But deflationary fears, central banks bond purchases and a ‘flight to safety’ from the rest of the world keep government borrowing costs down at unprecedented lows. Implicit here is ‘low to zero growth over decades’: a new version of Adam Smith’s stationary state. Only now it is the West that is stationary.

2. Economic Black Box: Financial Crisis, Financial Markets and Regulation

What is the biggest problem facing the world economy today? Where can we find the origin of the financial crisis that began in 2007? The first thing you can think of can be deregulation of the financial market that started from 1980s(specifically, Basel Committee 1988 accord that allowed very large quantities of assets to be held by banks relative to their capital, provided these assets were classified as low risk). That was what major influential thinkers diagnosed as a cause of the financial crisis. Paul Krugman, for example, argued that the repeal of Glass-Steagall legislation (enacted in 1933 for the tight control of banking where it separated commercial and investment banking) in 1999 during Reagan era helped to cause the crisis. He also argued the US had an era of spectacular economic progress – an era of ‘long period of stability after World War II with Glass-Steagall in place.’ The era was ‘based on a combination of deposit insurance, which eliminated the threat of bank runs, and strict regulation of banks balance sheets, including both limits on risk lending and limits on leverage, the extent to which banks were allowed to finance investments with borrowed funds.’

The author, however, disagrees both of Krugman’s claims. He argues that even with Glass-Steagall in force the crisis could have well happened and we cannot conclude the economy before Reagan-era is superior to that of deregulated era. He proposes that there were probably a few other factors at work in the changing productivity growth of the past seventy years: changes in technology, education and globalization.

Then, if not deregulation, what is the cause? The author argues that the problem lies not in deregulation but in bad regulation, especially in the context of bad monetary and fiscal policy. He claims that the financial crisis that began in 2007 had its origins precisely in over-complex regulation.

He raises two cases in this regard as complex financial regulation. First, the modern techniques of risk management were in many ways defective – especially when misused by people who forgot (or never knew) the simplifying assumptions underlying measures like Value at Risk. Second, he doubts whether additional regulation of the sort that is currently being devised and implemented can improve matters by reducing the frequency or magnitude of future financial crises. The answer is clear No. Further, he believes that the new regulations may have precisely the opposite effect.

He argues what matters is not the question of ‘Should financial markets be regulated?’ but rather of ‘What kind of financial regulation works best?’ He disagrees on the balance of opinion favouring complexity over simplicity; rules over discretion; codes of compliance over individual and corporate responsibility. He believes this approach is based on a flawed understanding of how financial markets work and asserts that excessively complex regulation is the disease of which it pretends to be the cure.

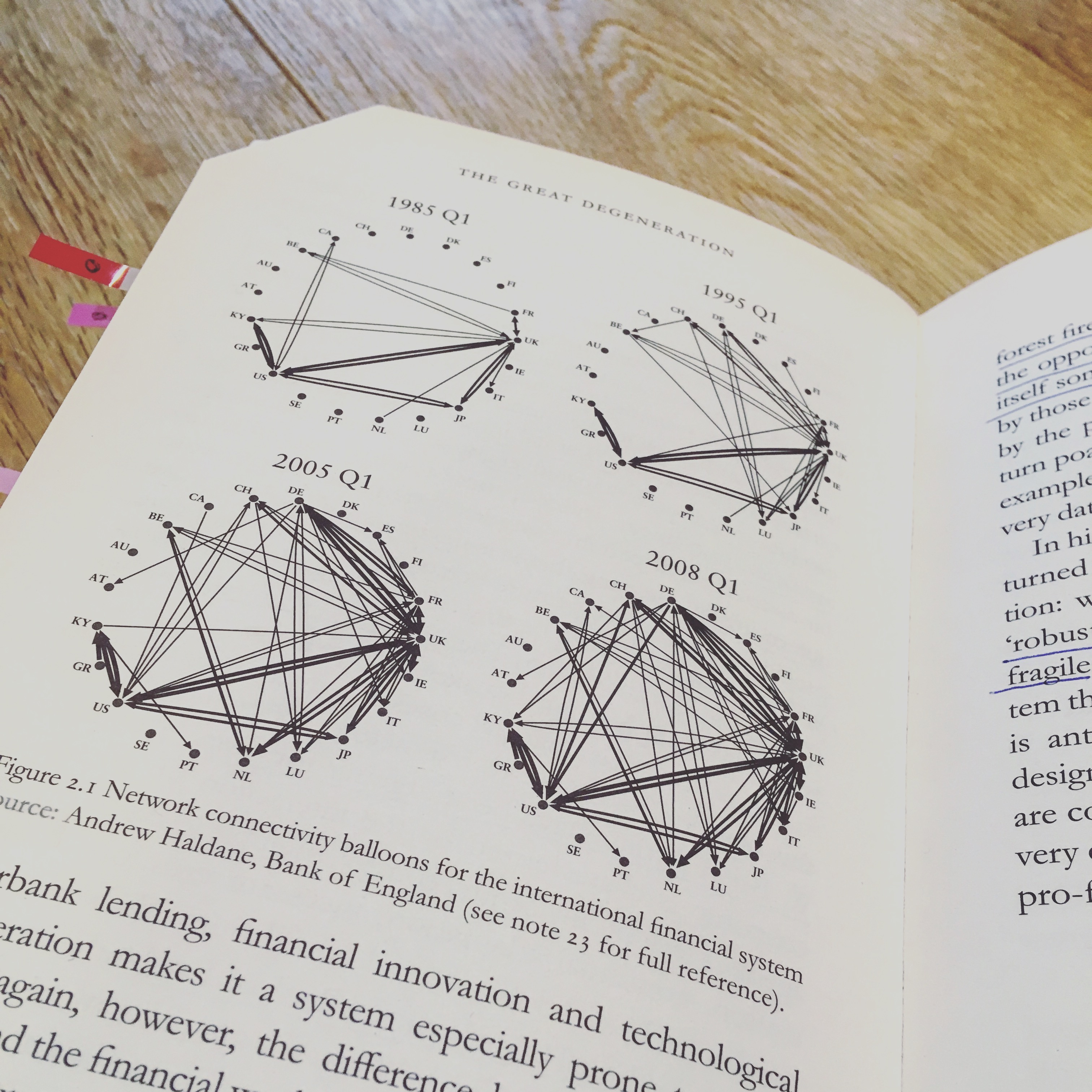

How does the financial markets work? The author brings to us two ways of seeing the financial markets to find the clue for ‘what kind of financial regulation works best.’

First way of understanding the financial market is a Darwinian evolutionary system as in the natural world where individuals and firms are in a constant struggle for existence, a contest over finite resources. The author illustrates six common features shared by the financial world and a true evolutionary system of the nature. Here, he also highlights the financial evolutionary process has been subject to big disruptions, as in the natural world, in the form of geopolitical shocks and financial crises.

The difference is, of course, that whereas giant asteroids come from outer space, financial crises originate within the system. The Great Depression of the 1930s and the Great Inflation of the 1970s stand out as times of major discontinuity, with ‘mass extinctions’ such as the bank panics of the 1930s and the Savings and Loans failures of the 1980s.

Another difference is whereas evolution in biology takes place in a pitiless natural environment, evolution in finance occurs within a regulatory framework where ‘intelligent design’ plays a part. Thing is, as per the author, this design in the financial market is not intelligent enough – even to make a fragile system even more fragile.

Second way of understanding the financial market is as a highly complex system, made up of a very large number of interacting components that are asymmetrically organized in a network. This network operates somewhere between order and disorder – on ‘the edge of chaos’. Such complex systems can appear to operate quite smoothly for some time, apparently in equilibrium, in reality constantly adapting as positive feedback loops operate. But there comes a moment when they ‘go critical’. A slight perturbation can set off a ‘phase transition’ from a benign equilibrium to a crisis. This is especially common where the network nodes are ‘tightly coupled’. When the inter-relatedness of a network increases, conflicting constraints can quickly produce a ‘complexity catastrophe’.

The author argues that financial crises are much the same. As W. Brian Arthur has been arguing for years, a complex economy is characterized by the interaction of dispersed agents, a lack of any central control, multiple levels of organization, continual adaptation, incessant creation of new market niches and no general equilibrium. And the combination of concentration, interbank lending, financial innovation and technological acceleration makes it a system especially prone to crash.

And again, the difference between the natural world and the financial world is the role of regulation. Regulation is supposed to reduce the number and size of financial forest fires. Yet, it can quite easily have the opposite effect. This is because the political bodies can be captured by those whom they are supposed to be regulating, not least by the prospect of well-paid jobs should the gamekeeper turn poacher. They can also be captured in other ways – for example, by their reliance on the entities they regulate for the very data they need to do their work.

The author borrows a great insight from Nassim Taleb’s book Antifragile. The opposite of fragile is not ‘robust’ or ‘strong’, – because those words simply mean less fragile – but is ‘anti-fragile’. A system that becomes stronger when subjected to perturbation is anti-fragile. In this sense, he argues that regulation should be designed to heighten anti-fragility. But the regulation we are contemplating today does the opposite: because of its very complexity – and often contradictory objectives – it is pro-fragile.

Lastly, in order for the effective application of the financial regulation, the author suggests to go back to the principles of Bagehot’s Lombard Street in two aspects.

First, we must ensure that those who fall foul of the regulatory authority pay dearly for their transgressions. The author argues those who believe this crisis was caused by deregulation have misunderstood the problem in more than one way. Not only was misconceived regulation a large part of the cause. There was also the feeling of impunity that came not from deregulation but from non-punishment.

Second, instead of exhausting ourselves drawing up hopelessly complex codes of ‘macro-prudential’ or ‘counter-cyclical’ regulation, we need to go back to Bagehot’s world, where individual prudence – rather than mere compliance – was the advisable course, precisely because the authorities were powerful and the crucial rules unwritten.

3. Legal Black Box: The Rule of Law

Following political and economic facets of institutional degeneration, the author discusses on the health of the Western legal system.

The author quotes seven key criteria defined by Tom Bingham, the late Lord Chief Justice and suggests the rule of law in England in his Bingham’s sense of the term is the products of historical evolution starting from Magna Carta in 1215 culminating with the Glorious Revolution.

He states that like democracy, the rule of law may be good in its own right but also good because of its material consequences: It is conducive to economic growth particularly insofar as it restrains the ‘grabbing hand’ of the rapacious state.

The author quotes insights of Douglas North who highlighted the importance of the ability of societies to develop effective, low-cost enforcement of contracts and of enforcement of contracts by a third party. His definition of the third-party enforcement is the development of the state as a coercive force able to monitor property rights and enforce contracts effectively. The author emphasizes that constraining the state to use its power of coercion in such as way as to respect private property rights is the essential function of the rule of the law in economic perspective.

The author suggests, compared to the civil law, the common law system, despite its shortcomings, offers greater protection for investors and creditors, with its trait of adapting to changes over time. He argues the authentically evolutionary character of the common law system is an advantage in terms of economic development.

However, he identifies a few distinct threats to the rule of law in the West, such as civil liberties eroded by the national security state, the growing complexity(and sloppiness) of statute law, and the mounting costs of the law especially in the US.

What the author observes, especially in the US, is what Mancur Olsen argued: Over time all political systems are likely to succumb to sclerosis, mainly because of rent-seeking activities by organized interest groups. In this angle, the author claims that while the United States was the rule of law in the past boasting proudly of their system as the benchmark for the world, now what we see is the rule of lawyers.

He further argues that the system is facing challenges for reform because there is so much that is rotten within it: in the legislature, in the regulatory agencies, in the legal system itself. The answer is that the reform should come from outside the realm of public institutions – i.e. from the associations of civil society: the citizens.

4. Social Black Box: The Civil Society

Is it possible for a truly free nation to flourish in the absence of the kind of vibrant civil society we used to take for granted?

The author believes in the power of the voluntary association without any public sector involvement just as Alexis de Tocqueville observed and praised the vibrant non-political association’s role in nineteenth-century America’s democracy.

However, the author states the vibrant civil society and social capital have significantly declined especially between around 1960s and the late 1990s as per Robert Putnam’s argument – ‘Putnam’s law of declining social capital’.

While Putnam saw the primary reason of the decline of the civil society and social capital being technology such as television and then internet, the author takes a different stance. For example, the online community such as Facebook creates social networks that are huge but weak, and he believes they cannot be a substitute for traditional forms of association and are not the reason that hollowed out the civil society.

Instead, he argues, it’s the state with its seductive promise of ‘security from the cradle to the grave’. He points out the public school system, as an example, that consequently deteriorated the competition and hence the quality of education, from which he sees that governments encroached too far on the realm of civil society for the past fifty years. He argues that the spontaneous local activism by citizens is better than central state action not just in terms of its results, but more importantly in terms of its effect on us as citizens.

He believes that true citizenship is not just about voting, earning and staying on the right side of the law. It is also about participating in the ‘troop’ – the wider group beyond our families – which is precisely where we learn how to develop and enforce rules of conduct: in short, to govern ourselves. To educate our children. To care for the helpless. To fight crime. To keep the streets clean.

CONTEMPLATION: A SHORT BOOK WITH YET STRONG IMPACT POSITIVELY AND NEGATIVELY

It’s true that there has been much intellectual discourse that tries to illuminate why poor nations are poor whereas not much attention has been given to why good institutions gradually get worse.

Certainly, as of the author’s writing in 2012, 4 years into the post-crisis recession, no clear sign of recovery was seen in the West despite massive public spending by the governments to prevent contraction of the economy. At the centre of the long debate among leaders was lost or disappeared productivity that was negatively affecting the growth. Also, much blame was made to deregulation that somehow helped cause banks’ reckless risk taking and moral hazard. In this situation, it’s natural to seriously ask WHY. Has the West lost its edge in their workings of institution? What is happening?

The answers are exactly made by the author through this brilliant book. Even though diagnoses made are somehow confined in the author’s conservative viewpoints, the author’s astute insights centred on four key institutional frameworks are stunning.

I believe readers would be taken aback to find similarities between what’s happening in our time and what was described as symptoms of the stationary state in the eighteenth century. Especially so when we look into the post-crisis West, the US specifically, in terms of reduced social mobility, widened income distribution and stagnant growth. We are warned.

Clearly, this book makes readers think. But more importantly, this book challenges readers especially when he shares his blunt criticisms in conservative narrative.

I have experienced a bit of difficulty in building a balanced perspective. While I greatly enjoyed the author’s intellectual elaboration with many great thinkers’ discussions, often times I found myself to get defensive in certain arguments he makes.

I will share what I’ve enjoyed from this book first and move on to what I didn’t enjoy.

What I Enjoyed

First, this book confirmed me that he is indeed a contrarian. It seems he doesn’t mind speaking his truth, so to speak. No beating around the bush. People may or may not agree on his viewpoints fully or even partially. But I believe he provides a valuable perspective that many (or majority) of influential minds may disregard. And that’s meaningful. We always have to have diversity of opinions in order to view the situation correctly and this is exactly what the author is doing, hence what makes this book remarkable.

Second, his ability to weave ideas of great thinkers through long historical context is intellectually pleasing. His scope is far and wide. Given my background in banking and finance, personally I was glad that I could learn about the common law system’s evolution through history and what the rule of law should be.

His emphasis on why institution matters and his warnings on potential problems when the balanced self-reinforcing inner workings of the institutions fail again reminded me of the importance of the subject. As I came to admire Daren Acemoglu through his fine work Why Nations Fail, the author’s main elaboration based on (or similar to) Acemoglu strengthened my belief on this issue.

His elaboration on how to understand the financial market in terms of Darwinian Evolutionary System and of Complex Adaptive System was terrific and again confirmed what other great authors/investors such as Mauboussin and Dalio believe. He made a good case on what’s different between the financial market and these two systems of the nature and hence how financial regulation has to be based on this difference. Such a great insight. I thoroughly enjoyed this part.

Also, his argument on why complex regulation is bad and can be counter-productive provided me another good chance to ponder on this issue. Actually, this aspect has been raised by a few other authors as well such Mervin King and Dale Carnegie Training. Regardless of his conservative viewpoint, I believe this issue is something we can look into.

What I Didn’t Enjoy

Despite these attractive attributes the book carries, the book has some shortfalls.

He is bold, sometimes provocative, and doesn’t hide what’s on his mind as I mentioned earlier. One of critical aspects that makes me hesitate to call this book great, is his stances in seeing the world. He clearly divides the world: The West versus the Rest. The English-speaking Common Law System versus the Others. The superior system versus the others, and so on. And it seems he wouldn’t mind being himself this way.

Can he provide more holistic viewpoint? Not the evolution of the West versus the Rest but the evolution of humanity on the earth overall? Even if it’s not our business that the author aims at just some specific readership who shares same value, I sincerely hope to see more accommodating view than this exclusivity. And we know there is a term called a ‘confirmation bias’. If his view is rather pre-defined in certain frame, the world may fit into his own bias rather than as it is. That can be bad for readers.

Another caveat I found is a bit personal. I tend to observe a dominant use of certain words. Disappointingly, the finding is not very attractive: Such words as colony, empire, superior, glory, etc. are quite frequent. Are we living in the past? I believe it’s an individual reader’s role to exercise a critical reading and take what’s only necessary for his evolution rather than to be swept by the ideas. You should be prepared when reading this book.

In the end, however, this very aspect is what challenges you, grows your ability to think critically and builds your own perspective. And it certainly helped me to see certain issues in new broadened perspective. That’s a good thing and I appreciate that.

Where is your country heading? Looking back what Adam Smith prescribed to cure Chinese stasis and also to reform the British Isles and its American colonies for galvanizing their economy – more free trade, more encouragement for small business, less bureaucracy and less crony capitalism – I can’t help but believe it’s an opportune time for us to look into our own long-sealed black boxes.

CLOSING

It’s the matrix of institutions where each of them should complement and reinforce the rest for a nation’s success. The institution in our times, however, are out of joint. To restore them and hence to return to those first principles of a truly free society, the author guides us to look into four key institutions that clearly show signs of degeneration – the government, the financial market, the law and civil society.

This brilliant book is full of intellectual ideas shared by great thinkers through history let alone of the author’s bold and yet provocative claims. Despite apparent shortfalls of this short book, his sharp insights and ability to juxtapose our times with those of Adam Smith in terms of the Stationary State function as a wake-up call to all of us.

I believe this book can provide a good insight for a society who experiences a degeneration of institutional functioning and equally for a society who experiences economic growth or/and wants to level up their institutional functioning thanks to multiple examples studied by the author.

WHO SHOULD READ THIS BOOK:

Economists, Policy Makers, Leaders in Banking and Financial Services, Politicians

RATING: 3 out of 5

RECOMMENDED CATEGORIES:

Business, History, Finance, Economics, Politics, Financial History, Economic History

ABOUT THE BOOK

Author(s): Niall Ferguson

Published: 2012, Great Britain

Publisher: Allen Lane, Penguin Group

Paperback, 152 pages

Reference:

2. General Government Gross Debt in percentage of GDP. Chart created from data from IMF on Oct 17th, 2018 by Jay: https://www.imf.org/external/datamapper/GGXWDG_NGDP@WEO/BEL/IRL/ITA/ESP/USA/GBR/PRT/JPN/GRC/DEU/FRA?year=2023